Updated June 2026

What Is Uninsured Motorist Coverage Insurance?

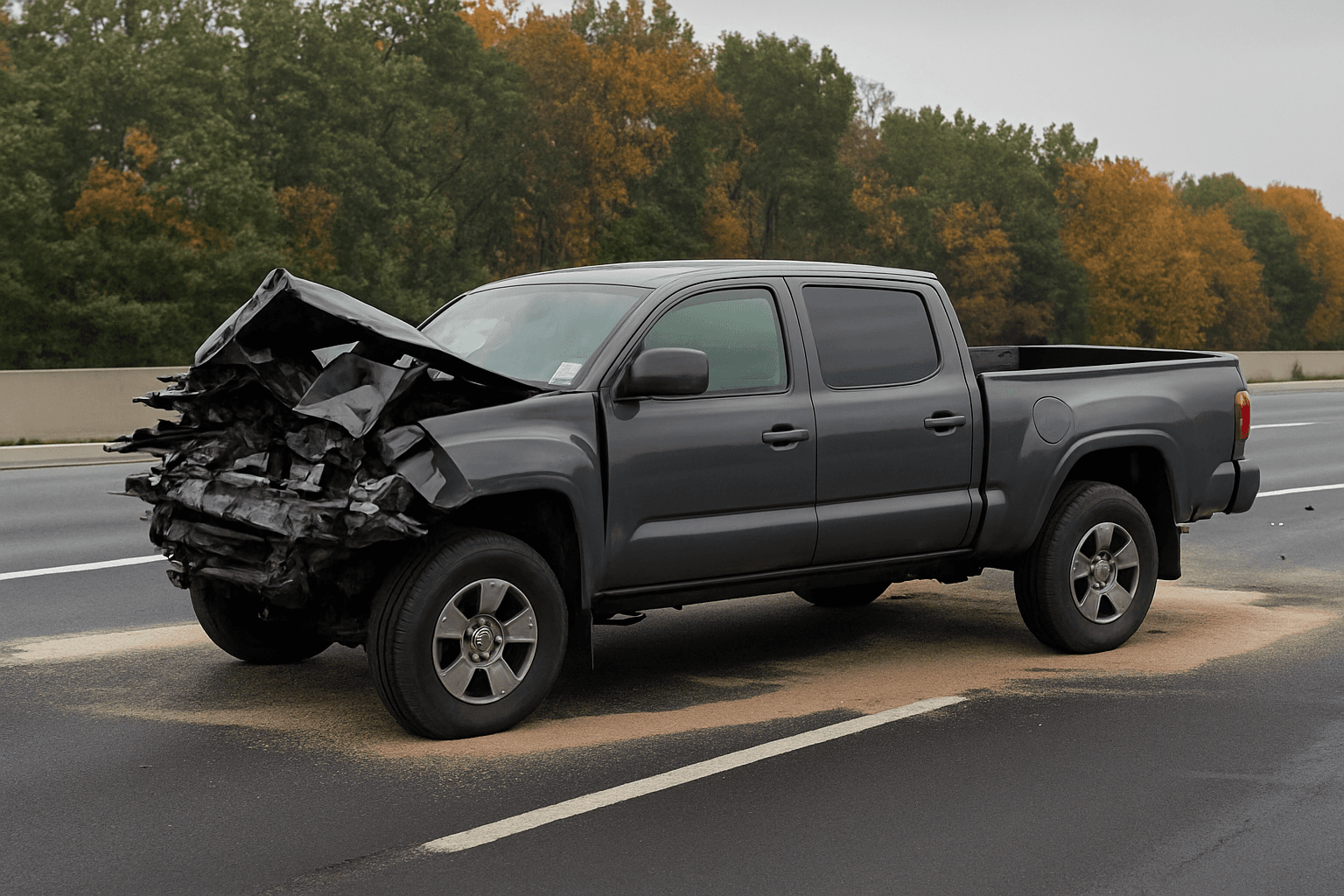

Uninsured Motorist Coverage pays for your injuries and vehicle damage when you're hit by a driver with no insurance, insufficient coverage, or who leaves the scene. Arizona law requires every carrier to offer UM coverage at the same limits as your liability policy—$25,000 per person and $50,000 per accident minimum. You can reject it, but only by signing a specific waiver form. If an uninsured driver rear-ends you and causes $8,000 in medical bills and $4,500 in car damage, your UM coverage pays both after you file a claim with your own carrier.

- You're stopped at a light in Phoenix when an uninsured driver runs the red and T-bones your car. You have $15,000 in medical bills and $9,000 in vehicle damage. The other driver has no insurance. Your UM coverage pays the $15,000 in medical costs up to your policy limit and the $9,000 vehicle repair under your Uninsured Motorist Property Damage portion. Without UM, you pay out of pocket or sue the driver directly—most uninsured drivers carry no collectible assets.

- Your car is parked outside your Mesa apartment when another vehicle sidesipes it and flees. Damage totals $6,200. You file a police report but the driver is never identified. Your UM property damage coverage pays the $6,200 repair minus your deductible because Arizona includes hit-and-run under UM definitions. Collision coverage would also pay this claim, but if you carry liability-only plus UM, the UM property damage component covers it.

- A driver with minimum liability limits—$25,000 per person—causes an accident that leaves you with $60,000 in medical bills. Their liability pays the $25,000 maximum. Your Underinsured Motorist coverage, if you carry it separately or stacked with UM, pays the remaining $35,000 up to your UM policy limit. Standard UM does not cover underinsured gaps in all states—Arizona allows it but you must confirm your policy includes Underinsured Motorist as a rider or combined UM/UIM coverage.

Who Needs Uninsured Motorist Coverage Insurance?

Suspended-license drivers reinstating after a DUI, points suspension, or lapsed-insurance suspension should carry UM because you are statistically more likely to encounter uninsured drivers during the reinstatement period when you're driving on a restricted or hardship license. Drivers on SR-22 policies must carry at least state minimum liability, and accepting the UM offer at the same limits costs under $15 monthly while protecting you from the most common claim scenario—being hit by another high-risk or uninsured driver. Non-owner SR-22 policyholders also benefit from UM because it covers you as a passenger or pedestrian struck by an uninsured driver.

Accept UM bodily injury at minimum state limits if you carry SR-22 or are reinstating a suspended license—the cost is under $12 monthly and one uninsured-driver accident pays for years of premiums. Add UM property damage if you do not carry collision coverage and drive a vehicle worth more than $3,000. Reject UM only if you carry full coverage collision with a low deductible and the duplicate coverage does not justify the extra $8 to $15 monthly.

How Much Does Uninsured Motorist Coverage Insurance Cost?

Uninsured Motorist Coverage typically adds $8 to $18 per month to your premium in Arizona, or $96 to $216 annually, for minimum state limits of $25,000/$50,000.

- Your UM coverage limits—higher limits like $100,000/$300,000 cost $15 to $35 more per month than minimum $25,000/$50,000.

- Whether you add Underinsured Motorist (UIM) coverage on top of UM—combined UM/UIM policies cost 20% to 40% more than UM alone.

- Your ZIP code's uninsured driver rate—Phoenix and Tucson have higher uninsured motorist percentages than rural Arizona, which increases UM premiums by $3 to $8 monthly in metro areas.

- Stacking vs non-stacking—if you insure multiple vehicles, stacked UM combines limits across all cars and costs 15% to 30% more than non-stacked.

- Your driving record—carriers price UM based on overall risk profile, so suspended-license drivers and those with SR-22 filings pay 10% to 25% more for UM than clean-record drivers.

- Deductible on UM property damage—Arizona allows carriers to offer UMPD with a deductible, typically $250 or $500, which reduces the monthly cost by $2 to $5 compared to zero-deductible UMPD.